Insurtech — New Dogs With Old Tricks

The Disruption of the $5 Trillion Global Insurance Market

The majority of my time with Hillside Ventures was spent focused on the Insurtech Vertical — conducting market research, meeting with founders, professionals at incumbent insurers, etc. Within the industry, I was surprised to see how a seemingly small amount of tech could have such an outsized impact on accuracy, efficiency, and scale of insurance products/services.

Disrupting the ‘old guard’ has been a staple of the tech industry since inception. In 2022 it feels like there are tech companies taking over every major category and no stone has been left unturned. What will be the next wave of technological changes? What markets will they come in? What are the next major opportunities?

In my view, there is a massive opportunity in the near to medium term to focus on innovation in markets neglected in the current tech landscape. I suspect that many of the big companies over the next few years will come out of industries that have fallen to the back burner during the most recent technological revolution. As we look forward to the internet revolution and the companies of tomorrow, there are still entire sectors stuck in an age not yet consistent with what we think of as the “companies of today”. The Insurance market, despite the last couple of years of growth and progress, sits as one of the few remaining laggards of the ‘old guard’.

In industries with little disruption, large incumbent players, and antiquated systems, gatekeepers of the status quo are able to make technological implementation difficult. High barriers to entry (regulation, capital intensity, scale of incumbents, general complexity) have historically limited the volume of startups attempting to solve key problems within the insurance space.

Although difficult, I take the glass half full perspective here in that the lack of technological progress and high barriers to entry are the exact reasons why these industries could make for such considerable opportunities.

In a past industry overview I dove into debatably the largest, most antiquated sector of them all…government. Today, I will look into one with a similar status — insurance.

What is Insurtech:

At a high level, insurance is really just a means of protection from financial loss. An individual, organization, or business pays “x” amount of money on a consistent basis to ensure protection against the risk of an uncertain loss, “y”. If sum(x) for time period t >sum(y), then an insurance company generates a “float” of sum(x)- Sum(y).

In instances of successful claims, the insurer will pay the policy holder using the pool of scheduled payments that has been collected over time. The difference between the scheduled payments (aka premiums)and the claims paid out (sum(x) — sum(y)) is the “float”. This spread is ultimately invested in interest bearing securities and voilà, insurance companies make money on the money they have just made.

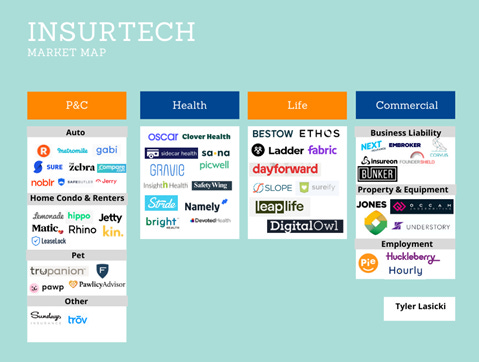

I tend to think of Insurtech companies as tech companies first, insurance companies second. Insurtechs develop the technology to improve insurance processes and outcomes. The traditional insurance functions that insurtech businesses commonly serve can be broken down into the following domains:

Insurtech startups have found ways to disrupt specific functions within each of the 3 major segments P&C, Health and Life, and Commercial. Many have thus far have focused on pricing/underwriting, claims processing, billing & other 3rd party admin functions. It is not uncommon for insurtechs that have proven they can contribute within one tier of the value chain to vertically expand their offerings and increase their usefulness across the full stack of insurance products/services.

Opportunity

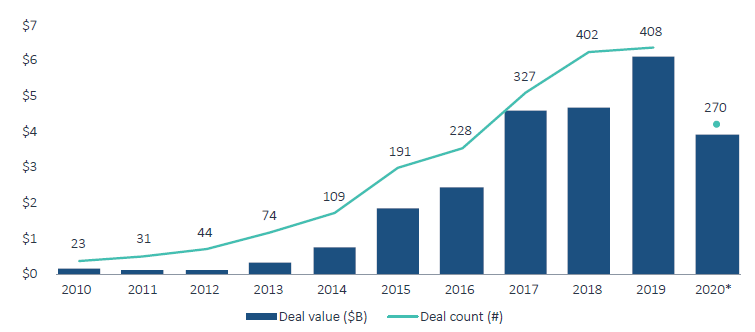

A McKinsey report highlighted that in 2011 just $140M was invested into insurtech companies. By 2015, $140M of insurtech funding had risen to $2.7B, in part due to seed and early stage startups maturing to advanced financing rounds. By 2019, greater than $6B had been invested and in 2021 that number jumped to a staggering $15.8B. Undoubtedly a massive jump in funding values, but in comparison to the broader insurance market which in 2019 alone wrote $1.32 trillion in insurance premiums, the funding has been just a drop in the bucket.

As an increasing portion of the VC and tech community is learning, a specific sector’s abilities to attract private market funding is not always an accurate indicator of the true potential of a given market. These funding values most correctly show how general investor interest in insurtechs has increased over time and how initial funding has led to larger rounds, helped create more mature companies, and has encouraged new talent to build in the space.

Over the last 18 months the first wave of insurtechs who have primarily focused on distributing insurance products, rather than building enabling technologies have gone public. The list includes Doma, Hippo, Lemonade, Metromile, Oscar, and Root. Collectively, they have not performed well in the public markets, some trading as low as 85% below last years price. Granted, this is in the midst of a broader public market tech correction* of which the Tech heavy Nasdaq is down ~30% from the November 2021 peak. This has made it difficult to gauge exactly how much of this poor stock performance is due to investor sentiment on overall public equities vs. the tech equities broadly vs. insurtech specific equities.

Based on public market performance and current investor sentiment as of June 2022, it is fair to assume that funding to insurtechs won’t be nearly as aggressive as it has been over the past three years. This will force insurtechs to focus on profitability and move to more sustainable business models.

Pictured below, is the loss ratio (gross and net) for Lemonade. Despite improving this metric from 166% in Q4 of 2017, it is still far higher than the industry average. A typically acceptable loss ratio sits within the 40%-60% range. Fundamentally, what this means is Lemonade is not charging customers for the risk they represent, a “growth at all costs” mindset. Loss ratios this high make it hard to be around for the long term; investors are cognizant of that today, much more than in recent history.

As a business model, selling technology to incumbent insurance companies is has gained recent traction. Globally, the IT spend of incumbent insurance companies has grown nearly 45% over the past 6 years. Although D2C insurtechs like Lemonade have found themselves reaching IPO status earlier than many B2B Insurtech providers — a massive opportunity also exists within B2B Insurtechs.

Trends to Watch

Partnerships Vs. Replacement

A large portion of insurtechs have shifted away from directly competing with incumbent insurance providers and instead have begun to partner with them. In fact, an argument can be made that much of the the insurtech growth and development has been because of incumbent insurers, rather than in spite of them. In an analysis of approximately 2,000 global insurtechs it was found that from 2010 to 2020, about one-third of them secured funding, and a handful established strategic partnerships with at least one incumbent.

91% of Insurtechs say they are not seeking to replace insurance giants like MetLife or State Farm, but rather fill in gaps to improve policyholder experience and/or make data more valuable. In fact, 61 percent of all insurtechs today offer their services to insurers.

There seems to be a symbiotic relationship budding between startups and legacy carriers as insurance companies are learning that they must embrace modernity and innovation to keep up with contemporary consumer demand. Insurtechs have similarly realized the value of leveraging existing customer bases, risk/pricing data, regulatory expertise, and scale of established players.

Embedded Insurance

Embedded insurance is the real-time bundling and sale of insurance coverage or protection when the risk is most top of mind for the buyer, at point of purchase. The 3 types of embedded insurance are the following:

“Soft” embedded services where customers can opt in to purchase insurance

“Hard” embedded services that come with an included warranty

Invisible embedded services, where the insurance is embedded into the unit price of a product or service

It has been found that including insurance as an add on at checkout has a conversion rate within the 20–50% range vs. a 2%–3% conversion when someone makes a purchase and seeks out insurance separately.

The ability to seamlessly integrate insurance products and solutions into customers’ digital journeys makes the buying process effortless for customers and extremely valuable for insurance providers.

Embedded Insurance Startups to follow: Route, Extend, Cover Genius, Element, Qover, and Boost.

Insuring “New” Risks

B2C Insurtechs like Hippo and Lemonade have figured out how to sell relatively the same coverage as the incumbent insurers, but in new/ innovative ways. Their competitive advantages have been:

Bypassing agents and acquiring customers and distributing insurance directly

Using data to personalize plans and offer more accurate/better pricing for customers

Automating much of the claim processes

Alternatively, there is an increasing cohort of insurtechs focused on insuring “new” risks ie: risks that are not covered by incumbent insurers. I like to to think of these “new” risks in two buckets:

New markets that incumbents have not modeled out products/services for (NFTs, e-scooter, drones/new mobility, cloud storage, etc)

Old/traditional markets that incumbents have pulled out from or disassociated with (Wildfire risk in CA)

Companies like Kettle, Delos, Coincover, Zego, Voom, and Paramterix all are tackling “new” risk areas.

At the core of all these companies is data. Each new risk insurer has innovative top of funnel data ingestion strategies that ultimately allow them to consider a larger array of factors per policy holder. This paired with innovative underwriting models allows these insurtechs to consider more criteria and run more efficient/accurate algorithms to process claims and ultimately assess and price risk.

As an example, in CA traditional insurers will asses homeowners wildfire risk using 2–3 data points. This ultimately results in mass denials of coverage for millions of homeowners. Insurtechs like Kettle and Delos are focused on creating more accurate wildfire risk models and have been able to create a competitive advantage by collecting greater than 200 data points per homeowner. Synthesizing climate data, satellite imagery, eco-regional factors, historical fires and losses, ignition insights, etc results in more accurate decision making and pricing.

Risks within Insurtech

Consumer Trust

Part of why insurance companies have persisted for so long is because they are stable, reliable, and rarely change — adjectives that juxtapose fundamentally what it means to be a startup. Creating authentic consumer trust is typically something that happens over long periods of time — a fact that investors don’t love to hear. Building consumer trust in young insurtechs is most definitely a barrier to entry.

For insurtechs with deep pockets, there is always the option of sponsoring every major sports team/event enough times until consumers believe you are a big and established company, cough* what every major Crypto exchange is currently doing.

Risk Accumulation in New Risk Markets

In all insurance markets, but specifically within “new risk markets” there is statistically speaking, a likelihood that all active policies will incur losses.

In unchartered territory like all “new risk markets” there are few, if any historical data sets to predict catastrophes and high tail-risk events. As new pricing and underwriting models are created, real data collected over time through experience becomes of increasing important in predicting these low likelihood, large impact events. Young companies may not yet have had time to accumulate large enough data sets to truly assess these kinds of risks — especially when the market is just getting on its feet.

Conclusion

Technological capabilities like comprehensive data collection, process automation, and ideas as simple as cutting out middle men are seen as table-stakes in most tech centric markets today. Within the insurance sector, these very characteristics have acted as points of differentiation and have created tens of billions of dollars in value.

In a market as slow moving and antiquated as insurance, seemingly small amounts of technological improvements have had an outsized impact on accuracy, efficiency, and scale of insurance products/services.

Even with the amount of technological progress, capital and growth in the insurtech space today, it could be said that the sector has almost found “product” market fit. Ie: The first wave of insurtechs that have hit the public market have proved that insurtechs provide a valuable service and that there is a market need for them. The next phase in the insurtech sectors lifecycle will be about finding the outliers who can sustainably grow with business models that can persist...